Underwriting Software Built by Insurance Professionals, for Insurance Professionals

Configurable underwriting software for insurers, mutuals, MGAs, and brokers with programs. Modular Solutions gives you enterprise-grade automation, security, a rating and rules engine, and refer-to-underwriter workflows — without the enterprise price tag.

Book a Demo

Book a Demo

What is underwriting software?

Underwriting software is the system used by insurers, MGAs, and brokerages with delegated underwriting authority to evaluate risk, price policies, and decide whether to bind, refer, or decline a submission. Modern underwriting software like Modular Solutions replaces outdated, manual spreadsheets and legacy tools with a configurable rating and rules engine, automation, and integrations – without any coding required. This empowers underwriters to quote faster, price more accurately, and maintain a clear audit and reporting trail across the policy lifecycle.

Underwriting Software & Policy Administration Ecosystem

Underwriting software is just one part of a larger policy administration ecosystem. This portion handles the quoting, rating, and decision whether to bind, refer, or decline a submission, including new business and renewals. This is the engine the rest of the insurance business runs on. In a modern policy administration ecosystem like Modular Solutions, underwriting is fully integrated with claims, finance, and distribution channels like broker portals and direct-to-consumer. It’s also made more efficient and accurate with automation, integration, and assistance from embedded AI.

Core Capabilities of Underwriting Software

- Rating and rules engine for simple and complex risks

- Refer-to-underwriter workflow with ability ro amend, accept, or decline

- Automated production of all documents including quotes proposals, applications, policy documents, declaration pages, wordings, and certificates of insurance

- Submission intake from email, PDF, and broker portal — increasingly AI-assisted

- Full policy lifecycle management – quote,bind, issue, endorse, cancel, reinstate, and renew

- Integration with third-party data such as sanctions, property data, vehicle information, and more

- Reporting and analytics across the book of business

Underwriting in Modular Solutions

Underwriting at Modular Solutions runs through the Policy Module. This is the command centre where your team manages the full policy lifecycle. It’s purpose-built for insurers, mutuals, MGAs, and brokers with programs who need carrier-grade underwriting capability without carrier-grade complexity.

A configurable rating and rules engine you control

Rates, rules, definitions, and wordings are configured in the Product Module. The moment you update them, the Policy Module picks up the changes automatically. No developers required. Eligibility rules, factor tables, surcharges, discounts, and weighted rating factors for mid-term changes are all configurable in-house.

Refer-to-underwriter workflows, built in

Submissions outside appetite or authority route automatically — or manually — to the right underwriter, with full context attached. Underwriters can amend, accept, or decline, and override coverage dates, premiums, commissions, or taxability when judgment calls for it.

AI-assisted submission intake

Our embedded AI assistant, ingests emailed and PDF quote submissions and structures the data automatically, eliminating manual entry and accelerating intake. Underwriters spend their time on judgment, not retyping.

The full policy lifecycle in one workflow

Quote, issue, endorse, cancel, reinstate, and renew from a single interface. Renewals can run automatically or be flagged for review — release as-is, release with changes, or lapse. Cancellations handle prorate, short-rate, returned premium overrides, and minimum or fully retained premium.

Automated document production

Quote proposals, applications, disclosure letters, declaration pages, wordings, registered letters, certificates of insurance, and proof-of-insurance — all generated automatically, all retained for audit.

Built-in integrations and the Solutions Exchange

Connect directly to the third-party data sources underwriters rely on such as sanctions screening, property and auto data, payment processors, accounting systems through our Solutions Exchange.

A work list designed for underwriters

Sort, filter, assign, set follow-ups, drag-and-drop attachments, and switch between Notes, Broker, Roles, and Reinsurer views. Role-based interfaces mean each user sees exactly the screen their job needs.

Reporting through the Intelligence Module

Loss ratios, hit ratios, conversion rates, and book-of-business segmentation live in the Intelligence Module — running on the same structured data your underwriters generate every day. Your data, your warehouse, full 24/7 access and ownership.

Why Insurance Leaders Are Replacing Legacy Underwriting Systems

There are three main reasons leaders at insurance companies, MGAs, and brokerages are considering replacing legacy underwriting systems:

- Cost.

- Capacity.

- AI readiness.

Cost of Legacy Systems

Not only are legacy systems often expensive, they may cost even more due to inefficiency and lost business. A lack of integration and automation causes many manual processes, lengthy workarounds, and/or duplicate entry. Slow response times can mean lost business. An inability to quickly update an existing product or launch a new program can result in missing opportunities in an increasingly competitive market.

The Capacity Squeeze

Reinsurance market conditions, rising loss costs, and increased competition mean underwriters need better tools to defend rate adequacy and prove discipline to capacity providers. Bordereaux that take a week to produce, books that can’t be sliced by class, and rating that can’t respond to a treaty change all undermine the relationship with the carriers and reinsurers your business depends on.

AI & Innovative Technology

Many legacy systems can’t adequately leverage new technologies such as AI. AI is only useful when it sits on clean, structured data. Many insurance organizations can’t unlock it because their underwriting data lives in unstructured email, PDFs or a disconnected system. Modern underwriting software fixes the data problem first and allows for AI to be effectively applied.

Underwriting Software for Every Part of the Distribution Chain

Underwriting software isn’t one-size-fits-all. Insurers, MGAs, and program brokers each carry different obligations to policyholders, capacity providers, and carriers — and the underwriting platform has to fit those realities. Modular Solutions is built for all three.

Underwriting Software for Mutuals & Insurers

Insurers and mutuals need underwriting software that handles the breadth of P&C — personal, commercial, farm, specialty, even Hutterite colonies and association programs — without requiring developers every time a product changes. Modular Solutions delivers the underwriting capabilities of a tier-one carrier at a fraction of the total cost of ownership. Configure rates, rules, and wordings in the Product Module and watch them flow into the Policy Module automatically. As a member and sponsor of CAMIC, we build with the community-driven values of Canadian mutuals in mind.

Learn more about Modular for Mutuals & Insurers →

Underwriting Software for MGAs

MGAs answer to capacity providers, and capacity providers want discipline they can see. Underwriting software for MGAs has to respect delegated authority, produce accurate bordereaux on time, and let you launch a new program without waiting on a vendor. Modular Solutions handles subscription and capacity management, automates bordereaux reporting and gives your team the rating, rules, and reporting depth your capacity expects. No code required to launch a new program or adjust an existing one. We’re a member and sponsor of CAMGA.

Learn more about Modular for MGAs →

Underwriting Software for Brokers with Programs

Program brokers occupy a unique position — managing programs like an MGA while serving clients like a brokerage. You need underwriting software that handles tiered commissions, delegated authority, and program-level capacity, while still keeping the broker side of the business productive. Modular Solutions runs the full program lifecycle on one platform: quote, bind, document, renew, and report — with optional direct-to-consumer distribution when the program supports it. Harvard Western Insurance issued 2,150 declaration pages and wordings in 30 days on our platform. Advantage Insurance manages over 1,500 client files in under two hours a day with a 95% reduction in processing time.

Learn more about Modular for Program Brokers →

The Underwriting Process in Modular Solutions

- Submission Intake – Submissions arrive via broker portal, email, PDF, or direct-to-consumer quote. Fully automate submissions with embedded AI.

Broker Portal Quote Submission

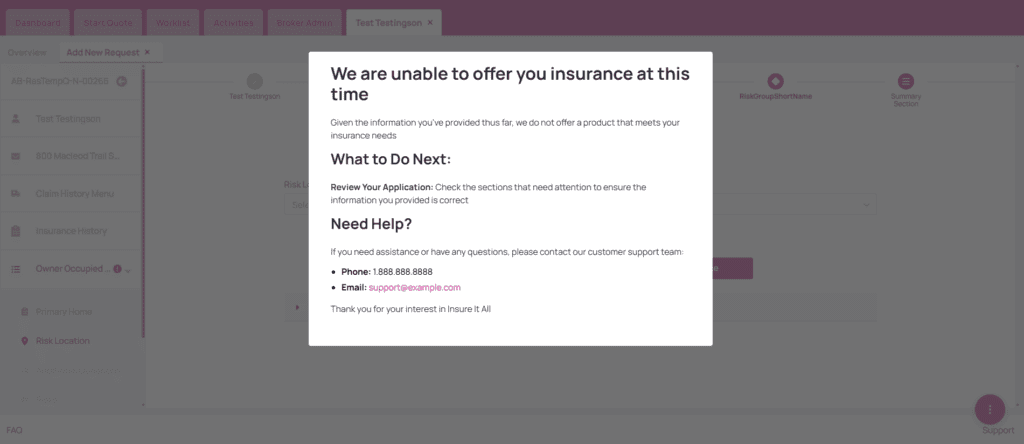

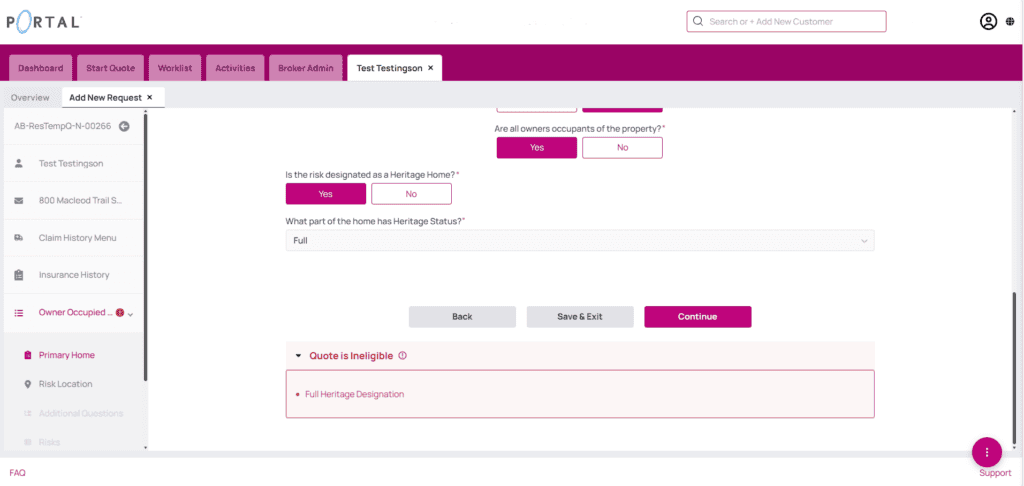

- Eligibility & Triage – Configurable rules check appetite, authority, and eligibility. Clean risks flow through; exceptions are referred to an underwriter.

Ineligible Message

Broker Portal Ineligible In-Quote Message

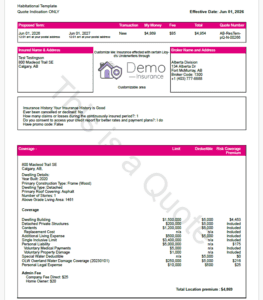

- Rate & Quote – The rating engine prices the risk and a proposal is generated automatically.

Sample Quote Proposal

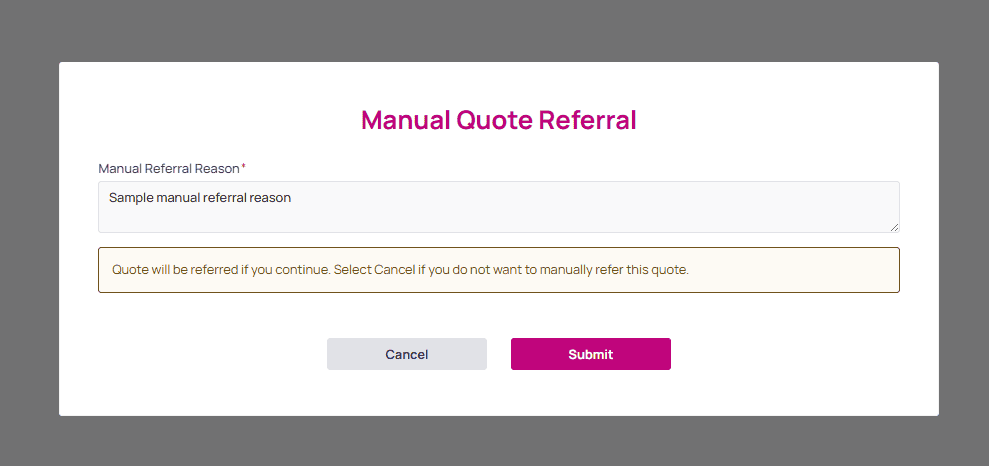

- Refer-to-Underwriter – For the risks requiring review, the right underwriter gets the file with all context attached.

Manual Referral

In-Quote Referral Message for Automated Referrals

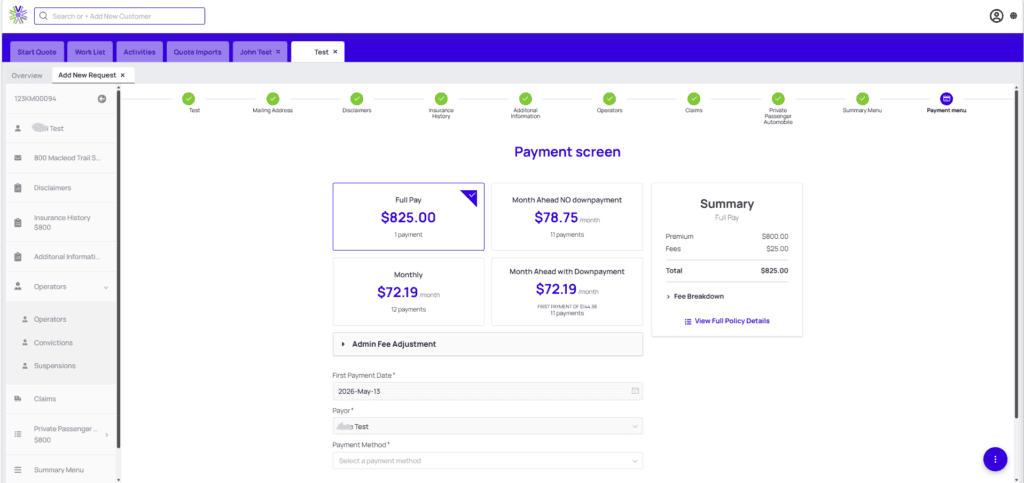

- Bind & Issue – Once accepted, process payment or setup premium financing in the platform. After payment, the system automatically issues policy documents, certificates, and confirmations; it also automatically emails them to the broker and/or client (depending on the configuration).

Payment Screen

- Manage the Policy Lifecycle – Endorsements, cancellations, reinstatements, and renewals all flow through the same configurable workflows in a single platform.

AI in Underwriting Software

AI delivers real value in underwriting software when it sits on clean, structured data and is incorporated to improve efficiency and accuracy. Our embedded AI assistant was designed to build on top of the platform’s data architecture. Here’s where that shows upin the underwriting workflow.

Submission ingestion.

Embedded AI parses email and PDF submissions, extracts structured data, and pre-populates the underwriting record. Hours of rekeying disappear and you can quickly and accurately generate quotes and proposals.

Surfacing the right information at the right time.

Embedded AI brings prior loss history, related submissions, and reference data into view as the underwriter works on the file.

Augmenting, not replacing.

AI handles the repetitive work; underwriters focus on judgment, relationships, and pricing strategy.

What Modular Solutions Underwriting Software Delivers

35%

Improvement in Underwriting Efficiency

95%

Reduction in Processing Time

20%

Increase in Automated Renewals

2150+

Declaration Pages Issued in 30 Days

“The platform allowed us to automate our underwriting process, applications, declaration pages, and bordereau reports which saves our team a substantial amount of time. The platform allowed us to automate applications for the issuance of 2150 declaration pages and wordings in 30 days. This policy administration system is a dream for brokers with programs.”

“We converted our policy management software to Modular Solutions in April 2024. Since then, we have experienced a 35% increase in underwriting efficiency and a higher degree of data validation. Their ability to create digital connections with other industry partners allows us to streamline processes which in turn, serves the people we exist for, our policy holders.”

Legacy Systems vs. Modular Solutions

Configuration: Vendor change requests, take weeks to months —- Self-serve option, no developers required

Submission Intake: Manual, rekeying from email or PDF —- AI-assisted parsing into structured data

Rating Changes: Coded, slow to deploy —- Configurable, deployable right away

Refer-to-Underwriter: Ad hoc, email-based —-Built-in workflow with full audit trail

Data Ownership: Vendor controlled, data hard to extract —- Your data, your warehouse, accessible 24/7

Total Cost of Ownership: High (license, customization, maintenance) —- Low – single platform, no per-seat surprises, maintenance included

Time to Launch New Product: Quarters to years —- Weeks

Security & Compliance: Built for Insurance

Insurance runs on trust between policyholders and carriers, between MGAs and capacity, between brokers and clients. The software underneath has to preserve this. Modular Solutions is built to meet the security expectations of regulated Canadian insurance organizations: data residency, layered defense, full auditability, and complete data ownership. We are proud to share Modular has completed a SOC 2® Type I examination, an independent review of how we’ve designed the controls that protect your data across security, availability, and confidentiality.

Canadian data residency. Cloud-hosted on Canadian soil with Tier 3 infrastructure, full redundancy, and elasticity — aligned to the data residency expectations of Canadian regulators and reinsurance partners.

2Zero-trust security model. Explicit verification, continuous identity posture monitoring, and least-privilege enforcement at every layer — not just at the perimeter.

3Encryption in transit and at rest. All data is encrypted using enterprise-grade key management. Unreadable to anyone without authorization.

4Role-based access controls. Users see only the data and functions their role requires — essential for delegated underwriting authority, segregation of duties, and broker portal hygiene.

5Strong authentication. Multi-factor authentication, password policies, and session management built in. No additional licensing required.

6Audit trails and logging. Changes are logged and traceable. Built for internal audits, regulator conversations, and reinsurance reviews.

7Infrastructure as code. Reproducible, version-controlled, and traceable environments. Every change is auditable.

8Your data, full access. 24/7 access to your production data via APIs and a structured warehouse you own — no vendor lock-in on the data your business depends on.

9Transparent subprocessors. Our subprocessor list is published and maintained — your procurement and compliance teams can review it before they ask.

Implementation & Support with a Canadian Team

The biggest risk in adopting new underwriting software isn’t the software — it’s the implementation. Prospects tell us the same thing in every conversation: they’re worried about multi-year projects, runaway costs, and platforms that never quite go live. Modular Solutions takes that risk off the table. Implementation is handled in-house by our Canadian team of insurance and technical professionals, and we’ve gone live on every project we’ve started. Our implementation success rate is 100%.

A Clear Implementation Path

We guide every customer through the same proven process: discovery, onboarding, product design and configuration, data migration from your legacy platform, custom development where needed, testing, training, and go-live. Each step has a named owner on our team and yours. Typical timeline is 12 to 18 months for a full insurer or mutual; smaller MGAs and program brokers often go live faster. Of course, this timeline depends on the number of products, their complexity, and the amount of internal team members you have dedicated to the project.

Implementation Services

Product Design & Configuration – Building your rates, rules, wordings, and underwriting guidelines in the Product Module.

Data Migration – Converting and validating data from your legacy platform onto Modular Solutions.

Custom Development – API integrations and additional features and functionalities specific to your business.

Training – UAT preparation, “train-the-trainer” sessions ahead of go-live, and a regularly updated library of documentation and video resources. We can provide additional training as well.

Ongoing Support – Our support desk is available from day one of launch, with weekly check-ins for the first several weeks post-launch. Tickets are triaged within 10 to 60 minutes and assigned to a named team member. Most resolve in 1 to 48 hours. Every three weeks, you receive release notes ahead of a production deployment, plus FAQs and help videos for any new functionality. You’ll never wonder what changed or why.

Underwriting Software Frequently Asked Questions

What’s the difference between underwriting software and a policy administration system?

Underwriting software handles risk evaluation, pricing, and the decision to bind, refer, or decline a submission. A policy administration system is broader — it covers the full policy lifecycle (quote, bind, issue, endorse, cancel, reinstate, renew) plus claims, finance, and distribution. Underwriting software is one part of a complete policy administration system. With Modular Solutions, underwriting lives inside an integrated platform; other underwriting tools may be standalone.

What features should underwriting software have?

Underwriting software should include the following features:

- Rating and rules engine that supports complex products

- Ability to refer to underwriters

- AI-assisted submission intake

- Ability to support the full quote-bind-issue lifecycle

- Integration with underwriting tools, data sources, distribution channels (broker portals and direct-to-consumer) and other pillars of policy administration such as claims and finance

- Reporting and underwriting analytics with full access to data

- Capacity and reinsurance management such as bordereaux reporting, subscriptions, aggregate limit tracking, and contract management

- Automated document generation and delivery

- Version-tracking, records, and capabilities for meeting audit and compliance requirements

The exact features and functionality required and offered will depend on the individual organization and software. Modular Solutions includes everything on the above list as well as additional features designed to support accuracy, responsiveness, and efficiency.

How does AI improve underwriting?

AI can improve underwriting through submission ingestion, surfacing the correct information, and handling repetitive, low effort tasks. This technology and its capabilities within underwriting are likely to evolve over the next few years. AI needs reliable, clean data to be effective and is meant to augment underwriters, not replace them.

Is underwriting software different for MGAs vs. insurers vs. Brokers?

Yes, underwriting software is different for MGAs, insurers, and brokers. Insurers and mutuals use underwriting software to build and price their own products, manage the full policy lifecycle, and report to regulators and reinsurers. MGAs use it to operate under delegated underwriting authority, manage capacity, and produce bordereaux for capacity providers — including Lloyd’s of London. Brokers with programs sit between the two: they manage programs like an MGA while serving clients like a brokerage, so their underwriting software has to handle delegated authority, tiered commissions, and broker-side workflows in one system. Modular Solutions is built for all three.

How long does it take to implement underwriting software?

Modular Solutions generally implements underwriting software in 12 to 18 months, but it can be faster for those with fewer or simpler products or programs. The exact length of time depends on the complexity and number of products and the amount of resources dedicated to implementation by the client.

Does Modular Solutions integrate with our existing accounting, broker management, or data vendors?

Yes, Modular Solutions integrates with a number of third-party vendors through the Solutions Exchange. This includes accounting, broker management, and data vendors. You can view a full list of our partners here.

If your existing platforms are not on this list, there is a possibility to create an integration. This is an additional cost and is dependent on API documentation and connectivity of the third party.

Where is our underwriting data stored, and who owns it?

Your underwriting data is stored in a structured data warehouse hosted on Canadian soil with Tier 3 infrastructure. You own the data and have full 24/7 access to it via APIs.

Can we configure rating and rules without a developer?

Yes, the ability to configure rating and rules without a developer is an exceptional feature of the Modular Solutions platform. Our platform does not require any coding or developers to make updates to existing products or build new ones. We do provide support if required, but your team can do this in-house.

How is Modular Solutions priced?

Modular Solutions has a two-part pricing model: a one-time implementation cost determined during discovery, plus an ongoing monthly subscription based on gross written premium transacted on the platform. Contact us for a quote tailored to your business.

See Modular Solutions in Action

Book a demo with someone who knows insurance. We’ll show you how underwriting works in the Modular Solutions platform and answer your questions.